With the recent disruption in the stock market due to Covid-19 and other world events, many are looking at the benefits of having liquid assets that can be accessible when needed and are not tied to the stock market.

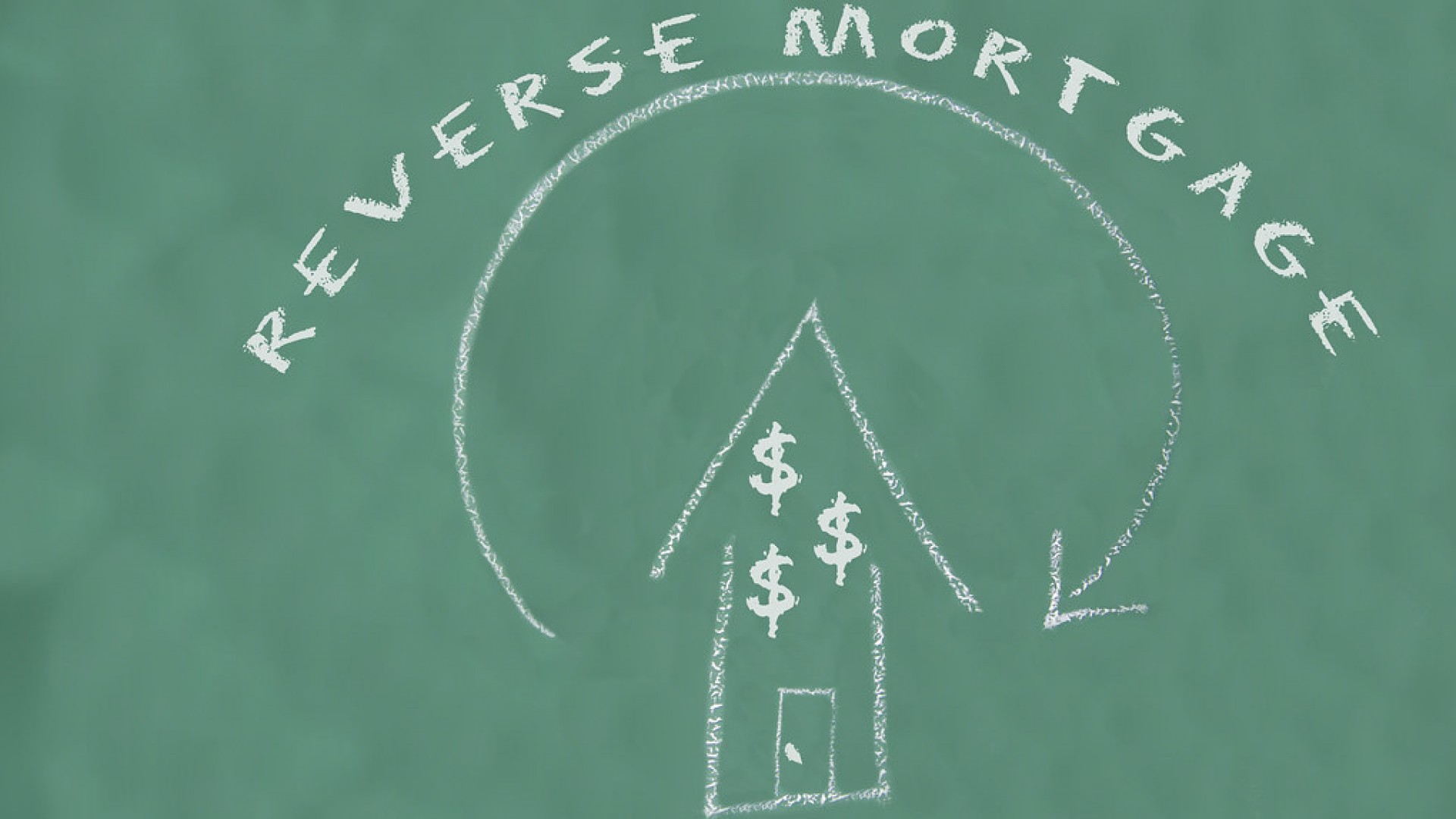

A reverse mortgage line of credit is such an option. Accessing some of your housing wealth to mitigate market downturns simply makes sense in an overall strategy to fund longevity in retirement. Buffer assets are those retirement funds that are tax-free and can come to your aid when market based funds disappoint. When the market is down is the very worst time to continue to draw from those sources and further deplete your portfolio especially in the first five years of retirement. Think about it... your projections for funding longevity are based on the growth of your retirement funds starting at the beginning of retirement. If the funds fail to perform, the outcomes will not be nearly as rosy and may result in running out of money too soon.

Having the option to implement a sequence of returns strategy allowing your portfolio time to recover is wise. Then, when the time is right, if you want to "repay" the reverse mortgage line of credit, you will lower the loan balance and replenish your line of credit simultaneously. The money in the line of credit is guaranteed to grow and compound annually at the same rate that the loan balance is growing. By "paying yourself" and replenishing the line of credit, you are providing a safety-net source of funds if needed again in the future as a buffer against a market downturn.

Homeowners who are 62 and older with 30% to 60% equity in their homes (depending on the age of the youngest borrower or non-borrowing spouse) are eligible. The home must be your primary residence and must have an FHA appraisal done in the process of the reverse mortgage.

Call (586) 753-9000

Credit and income requirements are easy because the program was designed to meet the needs of senior homeowners who are often on a fixed income. Many times, social security income is all that is needed, and even poor credit is often not a problem.

If you have a current mortgage, it will be paid off. Of course, you are still responsible for property taxes, homeowner’s insurance and maintaining the home. The sigh of relief for my clients who have eliminated their mortgage payment is audible! What would your life be like without a mortgage payment?

Contact me TODAY for the information you need to make an informed decision. Get the facts!

Call (586) 753-9000 We educate: YOU decide!